Most people think moving abroad is about palm trees and cheap beer. It's not. It's a financial strategy. And if you execute it correctly, it can be the single most impactful wealth-building decision you make in your lifetime.

I'm not being dramatic. I'm going to show you the math.

The Core Concept

If you earn in U.S. dollars and spend in a weaker currency, the gap between your income and your expenses widens dramatically. That gap is yours. You can save it, invest it, or compound it. Over 5, 10, 20 years, that compounding gap is the difference between being comfortable and being wealthy.

This isn't a hack. It's a structural advantage that millions of people have access to and only a savvy select few use it.

The Three Levers

There are three mechanisms that make this work. Most people only think about the first one. The real advantage comes from stacking all three.

Lever 1: Lower Cost of Living, Higher Savings Rate

This is the obvious one. You move somewhere cheaper, you spend less, you save more. But most people underestimate how dramatic the difference is.

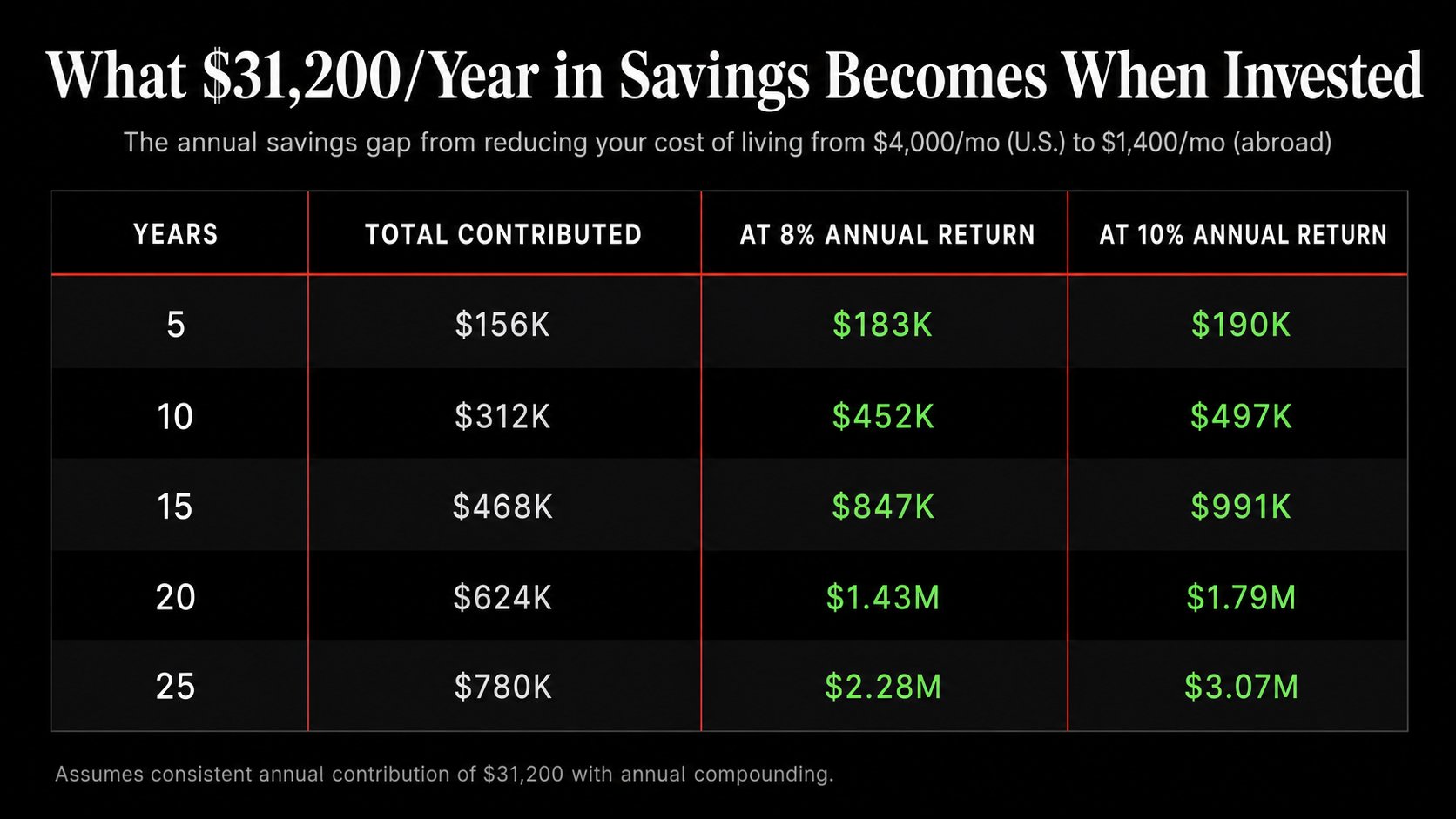

Here's a simple example. An American spending $4,000 per month in a mid-tier U.S. city. Rent, food, transport, insurance, the basics. No luxury. Just existing.

That same person moves to a city in South America or Southeast Asia and spends $1,400 per month. Better apartment, eating out daily, gym, health insurance, fast internet. Nothing about the lifestyle downgrades. Most of it upgrades.

That's $2,600 per month freed up. That's $31,200 per year in additional savings that didn't exist before the move.

Put that $31,200 into an index fund averaging 8-10% annually. After 10 years, that's roughly $500,000. After 20 years, it's over $1.5 million. Same income. Same job. Same salary. The only variable that changed was location.

The numbers speak for themselves. The gap between what you contribute and what you end up with is the compounding doing its job. And this is just one of the three levers.

Lever 2: Currency Arbitrage Over Time

This is the one almost nobody talks about.

When you earn in U.S. dollars and spend in Brazilian reais, Colombian pesos, Thai baht, or Vietnamese dong, you're not just benefiting from today's exchange rate. You're benefiting from the long-term trend of the dollar strengthening against most emerging market currencies.

Over the last 20 years, the U.S. dollar has appreciated significantly against nearly every currency in Latin America and Southeast Asia. That means your purchasing power in these countries has been increasing over time.

Let me put it simply. If you moved abroad 10 years ago and kept earning in dollars, the same dollar amount buys you meaningfully more today than it did when you arrived. Your income didn't change. Your cost of living effectively decreased because the currency you're spending in lost value against the currency you're earning in.

This isn't guaranteed to continue forever. Currencies fluctuate. But the structural forces behind dollar strength (U.S. monetary policy, reserve currency status, capital flows) have been consistent for decades.

You don't need to be a currency trader to benefit from this. You just need to earn in dollars and spend in something weaker. Geography does the rest.

Lever 3: Tax Optimization Through Strategic Residency

This is where it gets really interesting. And where most people leave the most money on the table.

Many countries have territorial tax systems, meaning they only tax income earned within their borders. If your income comes from the U.S. (remote work, investments, pension, Social Security) and you're a tax resident in a country with a territorial system, that income may not be taxed locally.

Some countries commonly discussed in this context include Panama, Paraguay, Costa Rica, and others with territorial or favorable tax frameworks. The specific rules vary by country, by income type, and by your individual situation.

There are also individuals who structure their lives to avoid establishing tax residency in any high-tax jurisdiction. They spend time across multiple countries, staying below the residency thresholds in each one. This is sometimes called the "flag theory" approach. It's legal, it's documented, and it's been used by internationally mobile professionals for decades.

The key point is this: where you live determines how much of your income you keep. Two people earning the same salary can have wildly different after-tax incomes depending on where they establish residency. That delta, compounded over years, is enormous.

The Compounding Effect

Here's where the math gets exciting. These three levers don't just add together. They compound on each other.

Lower cost of living means higher savings. Higher savings go into dollar-denominated investments that grow at 8-10% annually. The currency you're spending in weakens over time, making your existing savings stretch further. And tax optimization means more of your income reaches your investment accounts in the first place.

Stack all three and you're not just saving money. You're building wealth at a rate that would be nearly impossible in a high-cost, high-tax domestic environment.

This is why geographic arbitrage isn't a lifestyle choice. It's a financial strategy. And for people earning in strong currencies with the flexibility to live anywhere, it might be the most underutilized wealth-building tool available.

What This Looks Like in Practice

You don't need to be a digital nomad sleeping in hostels. You don't need to renounce your citizenship. You don't need to do anything extreme.

You need to pick a city where your dollars go further, whether that's Medellín, Lima, Bangkok, Da Nang, or dozens of other places across Latin America and Southeast Asia. Establish a comfortable life there. Keep earning and investing in dollars. And let the math work in your favor over time.

The people who actually do this aren't the Instagram backpackers. They're remote workers, consultants, retirees, and business owners who looked at the numbers and realized the smartest financial move they could make wasn't a new investment strategy. It was a new zip code.

Your Next Step

If you've read this far, you're already thinking about what this would look like for your situation. The specifics matter. Your income type, your tax obligations, your target countries, your timeline. Everyone's version of this is different.

I do free strategy calls every week. In 20 minutes we'll look at your numbers and map out what your move would actually look like, including where to go, what it'll cost, and how the math plays out for your specific situation.

If you're still early in the research phase, the Move Abroad Blueprint covers the foundational framework for geographic arbitrage, visa strategies for 7 countries, banking setup, and a 90-day action plan.

Get the Move Abroad Blueprint